Key Takeaways

- Stress testing is a systematic way to evaluate whether the financial (and other) expertise you use likely will deliver the results you expect.

- Eighty percent of single-family offices serving the Super Rich have done stress tests within the past five years.

- Your own stress-testing efforts can be comprehensive or focused on just one or two aspects of your financial life.

You can do thorough wealth planning and implement a financial product, tool or strategy only to end up with unexpected and disappointing results.

Why? Perhaps something about the strategy you implemented changed. Or maybe a new law was passed that impacted its effectiveness. It’s also possible that something occurred in your own life that made your current strategy insufficient or less than ideal. Let’s face it: Life isn’t static—and new developments can sometimes mean existing solutions no longer cut the mustard.

The Super Rich—those people with a net worth of $500 million or more—are fully aware of this. What’s more, they often take steps to avoid being surprised by negative or undesirable results from their wealth planning.

The good news: You can do the same thing, even if your bottom line is far smaller. Here’s how.

Stress testing at single-family offices

Some of the Super Rich have single-family offices to engage the very best professionals to help manage their finances and address lifestyle concerns. Single-family offices are organizational entities dedicated to the financial (and often personal) well-being of very wealthy families.

A major reason for the single-family office is to ensure the family is getting the best results possible. Consequently, one objective is to work with the best of the best. These professionals can be employees of the single-family office or external experts engaged to address specific matters.

The complication: There are times when even single-family offices are not working with the best of the best. Sometimes they end up working with Pretenders—well-intentioned professionals who are just not as technically proficient as circumstances require. But sometimes mistakes and oversights happen even when the very best professionals are engaged.

So what do these families do? To make sure they’re getting what they need and want in terms of expertise, services and solutions—and to determine whether those solutions remain on track to deliver expected results—the Super Rich and single-family offices engage in stress testing.

Stress testing is a systematic way to evaluate whether the financial (and other) expertise the family is using likely will deliver the results they expect and to ensure they are not missing any meaningful opportunities that could enhance their outcomes.

A popular approach

Stress testing generally is done because of anxiety about the current state of affairs. The Super Rich—as well as many other less-affluent families—might opt to stress test when they feel uncertain about their overall current financial or legal situation or about some particular aspect of their situation. By stress testing, a single-family office can help make certain that the family is indeed getting or employing the best solutions for their unique circumstances.

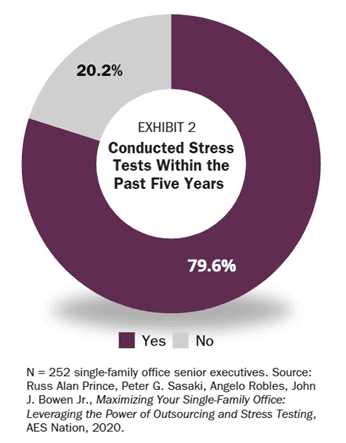

In a survey of 252 single-family office senior executives, about 80% of them engaged in stress testing within the past five years (see Exhibit 2). This demonstrates the pervasiveness of stress testing among even extremely wealthy families—who we find tend to employ some of the finest professionals available. Even those families and professionals are strongly inclined to make sure everything works the way they want it to.

Important

You don’t have to be extremely worried that something is amiss with a strategy before you engage in a stress test. Stress testing can be valuable even when the probability of something being wrong with a solution is quite low. Say, for example, that a mistake or error involving a particular strategy you’ve implemented likely would be extremely harmful to your financial well-being. It might make sense to stress test that strategy just to be certain that you’re not headed for a disastrous result.

Two types of stress tests

It’s important to note that stress testing is not one approach. There are actually two types of tests: comprehensive and focused.

Comprehensive stress testing involves many aspects of a family’s financial and nonfinancial lives. For stress testing to be considered comprehensive, we believe three or more particular sets of services or products initiated within the same 18-month period should be assessed. In contrast, focused stress testing involves fewer than three sets of services or products initiated in the same 18-month period. Often just one aspect of an overall wealth plan is tested at a time.

Comprehensive stress testing is much more involved, time-consuming and costly than focused stress testing. In contrast, focused stress testing is more targeted (and thus less expensive and time-intensive).

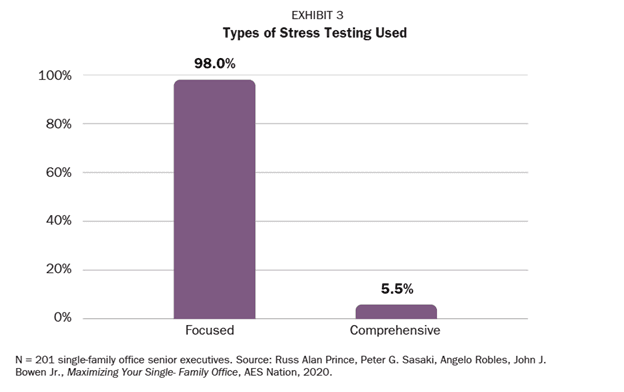

As seen in Exhibit 3, focused stress testing is far and away the more common approach used by single-family offices. Generally speaking, only when the single-family office is experiencing a system failure of some kind—something dramatic that impacts many aspects of a family’s world—is it likely to undertake comprehensive stress testing.

Finding faults

The goal of stress testing is to identify errors and missed opportunities. And it turns out that stress tests do identify these things fairly regularly. In the study, more than 40% of single-family offices found faults because of stress testing. Clearly, mistakes occur—even among top professionals. Thanks to stress testing, they potentially can be fixed before problems get serious.

Consider one hypothetical example of Super Rich-level stress testing. A stress test of a will discovered that a family’s youngest son, then 6 years old, was slated to receive an inheritance of slightly more than $250 million when he turned 12—a fact that surprised and dismayed the family. The problem was a simple typo: The will should have read that the son inherits the fortune at 21 years old, not 12 years old.

However, even correcting that error didn’t address the problem—as the family also didn’t want to give so much wealth at one time to a young adult. The stress test revealed that there had been a serious breakdown in communication between the family and the people involved in drafting their plan.

Because of the stress testing, the Super Rich family’s wealth plan was dramatically adjusted and updated. Now, the son will inherit substantial wealth in stages beginning when he turns 21. In addition, the wealth plan has a framework and structure for creating a dynasty while also insulating family members from losing wealth because of litigation or divorce.

Note

Stress testing at single-family offices can and often does extend beyond addressing wealth management and related legal matters. It can also be used to evaluate lifestyle decisions. For example, more of the wealthy are stress testing their family security measures—such as making sure their homes are truly well protected from burglars.

What’s that? You don’t have a single-family office?

Let’s assume you’re not a multimillionaire with your own single-family office. You can still engage in stress testing to help you determine whether your wealth management solutions remain on target to deliver the desired results. And you still can use stress tests to see whether there are any opportunities that you aren’t currently taking advantage of but should consider, given your goals and situation.

In other words, you can take a page from the playbook of the Super Rich and evaluate your current solutions. We also see that a growing number of professionals are becoming familiar with and adept at the stress-testing process. This is translating into more stress testing, which is a good thing. Many mistakes are just that—mistakes. They are unintentional but can have severe consequences. By stress testing, you can make sure the professionals you are working with are indeed getting everything right and you are not missing out on meaningful opportunities.

Some areas where we frequently see focused stress testing being done include investment portfolios, estate plans and business succession plans.

The upshot:

You can put some, many or even all aspects of your financial life through their paces to see whether they’re still set up to do what you want them to do and deliver the results you expect. If you take this step and engage in stress testing, you’ll be following in the footsteps of some of the wealthiest, most successful families—the Super Rich.

VFO Inner Circle Special Report

By John J. Bowen Jr.

© Copyright 2024 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including but not limited to electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the author nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The author will make recommendations for solutions for you to explore that are not his own. Any recommendation is always based on the author’s research and experience.

The information contained herein is accurate to the best of the publisher’s and author’s knowledge; however, the publisher and author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Nathan Brinkman is a registered representative and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC (www.sipc.org) Supervisory office: 8888 Keystone Crossing #1600, Indianapolis, IN 46240 (317) 469-9999. Triumph Wealth Management, LLC is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Nathan Brinkman: CA Insurance License #0C27168 CRN202805-8594422