Key Takeaways

- Don’t lose sight of key goals when making decisions about wealth.

- Avoid financial professionals who are merely pretenders— or worse.

- Don’t assume your plan is always on track—do a stress test now and again.

The Super Rich—those with a net worth of $500 million or more—tend to realize an important fact: The bad decisions and errors you avoid can be just as important as the savvy actions you take.

That’s often the case when it comes to building and maintaining serious wealth, in our experience.

The fact is, no one—not even the very wealthy or the most intelligent among us—is immune to making mistakes with their money. Various schemes, like the Ponzi scheme engineered by Bernie Madoff, have ensnared many affluent investors with their amazing promises.

That said, we find that many very affluent, highly successful people do tend to avoid certain crucial errors that might otherwise impact their bottom lines and financial futures. What’s more, these are the same types of mistakes that can trip up investors and families at just about any level of wealth. That’s actually good news, as it means you can potentially learn from the Super Rich how to avoid the mistakes that might threaten your own financial security.

The upshot: By paying attention to what the Super Rich don’t do with their wealth, you might just sidestep big problems—and potentially help your bottom line as a result.

Avoid these blunders

With that in mind, here are three of the biggest financial blunders that the Super Rich make a point to watch out for so they can avoid them.

Losing sight of goals

The Super Rich often establish family offices to address the many complex financial and personal objectives they have. Family offices can coordinate all the “moving parts” and are generally very skilled at helping Super Rich families develop and spell out their goals. They can even help their clients determine their deeper philosophies and beliefs about wealth and values—and how the two should be coordinated. They might, for example, craft a family vision statement about the family’s optimal outcomes and the reasons (both practical and psychological) for wanting them. Then they create a mission statement and a plan with the steps to take to realize that mission.

From there, all decisions about wealth are made only after considering the family’s vision, values and action plan. Any moves or changes should reflect those underlying factors. By having systems in place to never lose sight of their key goals and the factors underlying those goals, the Super Rich do a superior job of not chasing hot investments or opportunities that don’t amount to anything.

That doesn’t mean the Super Rich are rigid and inflexible when it comes to their wealth planning and financial decision-making. Without question, in order to adapt to changing circumstances—new developments in terms of what family members need, for example— high-functioning family offices are designed to be nimble and open to new paths. When goals change significantly enough, they make adjustments.

The big lesson:

Be very clear about what you want to accomplish. While it is important to be flexible, any decision to make adjustments or large shifts in strategy should be deliberate and carefully considered. Likewise, your decisions should certainly not be the result of a lack of guidelines for making smart decisions or because you’ve discovered a “shiny and new” investment product that has nothing to do with your financial goals, values and philosophy.

Working with professionals who are subpar—or worse!

Due to their rarified level of affluence, the Super Rich understand that a lot of professionals would like to have them as clients—but that not all of those professionals are worthy of consideration. Indeed, the Super Rich know better than most that there are far too many “professionals” who are actually:

- Pretenders—professionals with good intentions who aren’t particularly technically capable, especially when it comes to sophisticated solutions. Pretenders might care deeply about helping you but just can’t do it all that well and usually aren’t even aware of their limitations.

- Predators—criminals looking to use their guile and cunning to separate you from a percentage of your wealth.

- Exploiters—very smart professionals who often promote complex, legally aggressive financial solutions that may not prove viable. While these solutions are not illegal, there is a good possibility they will fail to deliver as promised at some point down the road (probably right when you need them to work!). Exploiters promote them because these solutions put a lot of money into their own pockets.

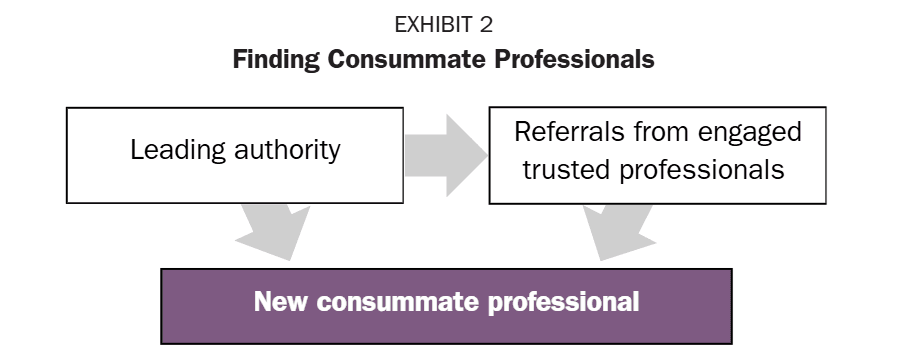

Often it’s hard to separate the good from the bad. So how do the Super Rich identify and avoid these three types of professionals? The most successful family offices serving the Super Rich take specific steps to help confirm they are working with consummate professionals (see Exhibit 2).

For starters, the Super Rich gravitate to leading authorities. Whether for senior management positions or as external providers, the objective is to work with recognized experts—such as industry thought leaders.

They also rely heavily on referrals when seeking out consummate professionals. The most consistently effective method is to garner referrals from high-quality professionals they are currently engaging. That’s because, generally, high-quality professionals tend to know other types of consummate professionals. Example: A top money manager likely knows elite wealth planners and leading insurance specialists who both are skilled and have integrity.

Finally, they’re willing to pay well for quality. While the Super Rich make a concerted effort to minimize costs, as we all do, they are not going to forgo desired results simply because pursuing those results might require them to spend some money. The Super Rich understand that it’s important to assess a provider not just on their stated fee but also on that person’s ability to deliver value.

The big lesson:

It’s essential to avoid pretenders, predators and exploiters when seeking out financial professionals to work with. By turning to leading authorities—thought leaders—and soliciting referrals from high-caliber professionals you already know and trust, you can potentially greatly increase your chances of working with a truly skilled professional—one who has both the willingness and the ability to get you to where you want to go in ways that don’t jeopardize your future.

Failing to get second opinions and do stress tests

Remember “Trust, but verify”—the phrase made famous by Ronald Reagan when talking about the Soviet Union? The Super Rich, especially those using single-family offices, take that message to heart. They are fully aware that even the top professionals they tend to hire can make mistakes. They also know that changes in their lives or the world at large can impact how a solution they have in place will behave. Therefore, the Super Rich rely on second opinions and stress testing.

Ideally, a second opinion occurs before action is taken. Example: Say a single-family office is considering a particular tax mitigation strategy for the family it serves. The office might get a second opinion from another noted leading tax authority to be certain about the validity and viability of the strategy. Second opinions are commonly obtained whenever there is any question or any sense of uncertainty, but really they can be sought at any time. For example, many investors (both Super Rich and otherwise) obtain second opinions about their overall financial strategy if they’re worried they might not be on the right track—or that the professionals they’ve enlisted aren’t up to snuff.

Stress testing is typically done when the Super Rich want to evaluate an existing strategy that’s already in place. It is a check to see whether what they implemented in the past remains (and is likely to continue to be) both viable and valid—that things are working as predicted. For many of the Super Rich, stress testing is like an annual medical checkup. There may not be anything wrong, but it is a very good way to catch a problem before that problem becomes severe.

The big lesson:

No matter your level of wealth, getting a second opinion when you are unsure or uncomfortable about a strategy, idea or product is usually worthwhile. Similarly, periodically stress testing your overall wealth plan or aspects of it can enable you to avoid problems now or down the road.

A comprehensive review

By and large, the self-made Super Rich have proved that they know what to do—and what not to do—in order to create, grow and maintain sizable wealth. By avoiding major slipups on your own path to wealth creation, you can potentially encounter fewer financial potholes along the way.

One way to get started implementing the best practices of the Super Rich: Consider getting a second opinion about the current state of your finances and how effective your current solutions are likely to be down the road. A comprehensive review of where you are today, where you want to be and the gaps between the two may indicate that everything is in its right place. But it could reveal issues that need to be addressed—and it makes sense to catch them sooner rather than later.

VFO Inner Circle Special Report

By John J. Bowen Jr.

© Copyright 2025 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including but not limited to electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the author nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The author will make recommendations for solutions for you to explore that are not his own. Any recommendation is always based on the author’s research and experience.

The information contained herein is accurate to the best of the publisher’s and author’s knowledge; however, the publisher and author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Nathan Brinkman is a registered representative and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC (www.sipc.org) Supervisory office: 8888 Keystone Crossing #1600, Indianapolis, IN 46240 (317) 469-9999. Triumph Wealth Management, LLC is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Nathan Brinkman: CA Insurance License #0C27168 CRN202809-9614530