Why save for college over a decade or more if you can front-load five years’ of contributions in a single year and let compounding work its magic? It’s called superfunding, and it’s a little-utilized way to save for private K-12 school and college.

Don’t fund your 529s like everyone else. A little-known IRS provision called superfunding lets you front-load five years of contributions in one move.

How the Gift Tax Rules Work (To Understand the Superfunding Exemption)

Every year the IRS releases an annual gift tax exclusion amount. Gifts to a beneficiary (which includes saving money in a college savings plan) that exceed the limit each year count against the taxpayer’s lifetime annual exemption, currently $15M per person. Gifts at or below the limit do not, and it’s a popular way to transfer wealth without dipping into your lifetime limit.

The 2026 annual gift tax exclusion is $19,000 per person, per recipient ($38,000/couple if they elect gift splitting). So, a married couple could give each child $38,000 without affecting their combined $30M federal gift tax exemption.

Superfunding Rules

There’s a special exemption to the standard annual gifting limits, but just for 529 plan contributions. Here’s how it works:

- Superfunding lets you contribute up to five times the annual gift limit to a 529 plan in one lump sum. So, in 2026, one person could save $95,000, $190,000 as a couple, and treat the contribution as if it were made over five years.

- A gift tax return is required for gift-splitting (Form 709) but in most circumstances, no tax is owed.

- The donor cannot make additional annual exclusion gifts to that beneficiary during the 5-year window without eating into the lifetime exemption.

- Superfunding is available to parents, grandparents, relatives, friends, etc.

Benefits of Saving for College with a 529 Plan

529 plans have several key benefits at the federal level (state tax rules may vary):

- Contributions grow tax-deferred (like an IRA or 401(k)).

- Investment growth is not taxed when funds are used to pay qualified educational expenses.

- Recent changes to 529 plans now allow parents to withdraw up to $20,000 per year to pay for K-12 private school and other educational expenses.

- Money leftover in a 529 plan can be rolled over to the beneficiary’s Roth IRA (tax free, lifetime limit $35,000, other rules apply) or the beneficiary can be changed to another family member.

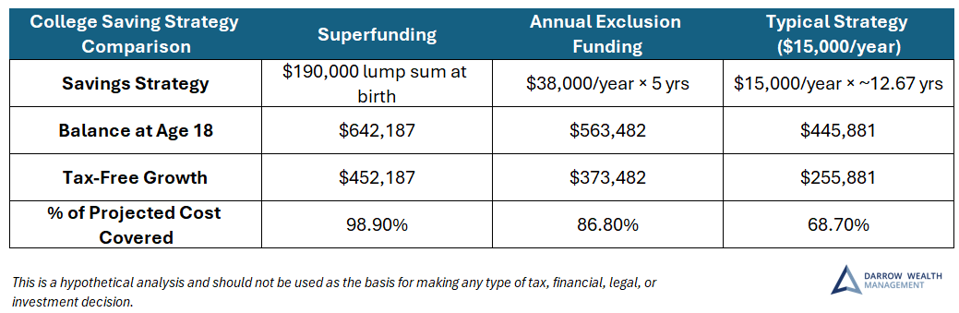

Saving for College at Birth: Here’s How the Strategies Compare

To illustrate the benefits of compounding, consider this hypothetical analysis. All three scenarios invest the same $190,000 in total, growing at 7% annually, but superfunding grows the account by nearly $200,000 more than spreading contributions over 12+ years, just from time in the market. In fact, the superfunding scenario nearly covers the cost of a private, four-year college education.

According to LendEDU, in 2026 the average all-in cost of a private nonprofit 4-year university is $62,570. If we assume that increases 5%/year until the child starts college at age 18 in 2044, the projected future cost is $649,028.

Superfunding a 529 Plan for College At Birth: Here’s How the Savings Strategies Stack Up

Kristin McKenna, CFP® Darrow Wealth Management

Who Should Front-Load College Savings?

Of course, having the cash to superfund a 529 plan is essential to making this strategy work or even being able to consider it. But for parents with young children expecting a major liquidity event , this can be a compelling way to invest a portion of the proceeds.

Even though there are new opportunities to use money in a 529 plan without paying tax on investment growth or a 10% penalty, parents (and other donors) should still consider the entire situation before maxing out a 529 plan.

Here Are Some College-saving Considerations

- The cost of college ranges dramatically between universities, which will determine how well-funded an account is.

- Private school K-12 can reduce the risk of over-funding a plan.

- Graduate school, medical school, and other advanced degrees are even more reasons to superfund.

- Families should consider coordinating contributions and the overall funding strategy, even if the money is held in different accounts.

- If you’re getting a late start, it might not make sense to use a 529 plan. Instead, consider another exception to the annual gifting limits: when payments are made directly to a qualifying educational institution, it does not count as a gift at all (no annual exclusion, lifetime limit, or Form 709 filing). This only covers tuition, but it’s still a key benefit.

Superfunding a 529 isn’t a complicated strategy — but it requires cash and planning. The families who benefit most are those who act early, coordinate contributions across generations, and think about the 529 as one piece of a broader education funding plan rather than a standalone account earmarked for one purpose.

By Kristin McKenna, Senior Contributor

© 2026 Forbes Media LLC. All Rights Reserved

This Forbes article was legally licensed through AdvisorStream.

Information from third parties may be proprietary, privileged and/or confidential, any use, copying, retention or disclosure is strictly prohibited. Securities and investment advisory services offered through qualified registered representatives of MML Investors Services, LLC, Member SIPC. The views and opinions expressed are those of the author(s) and may not accurately reflect those of MML Investors Services, or its affiliated companies. Local firms are sales offices of Massachusetts Mutual Life Insurance Company (MassMutual), and are not subsidiaries or affiliates of MassMutual, MML Investors Services, or their affiliated companies.

Nathan Brinkman is a registered representative and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC (www.sipc.org) Supervisory office: 8888 Keystone Crossing #1600, Indianapolis, IN 46240 (317) 469-9999. Triumph Wealth Management, LLC is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Nathan Brinkman: CA Insurance License #0C27168