Key Takeaways

- Luck plays a bigger role in the outcomes we achieve than we may want to admit.

- Calibrate the likelihood of achieving a goal you’ve set for yourself, your division or your company.

- Contingency planning and greater flexibility can potentially help you if your probability of success is low.

Because we like to neatly categorize things and bring a sense of order to our life, it’s very common for many of us to think about things in rigid, black-and-white terms.

For example, in our experience, lots of entrepreneurs and executives boil down the situations they encounter in the business world to simplistic yes-or-no outcomes. They might view a potential sale by asking, “Will the client buy or not?” They might approach a negotiation by asking, “Will the deal close or not?” And they might assess a new job opportunity by asking, “Will I get the position or not?”

While that approach makes intuitive sense on a certain level, it’s actually not all that valuable in sizing up opportunities and challenges. Tellingly, it’s not how most of the self-made Super Rich—those with a net worth of $500 million or more—tend to think.

Instead, the Super Rich have a habit of thinking about professional dealings in terms of probability—when assessing a situation, they ask, “What are the odds?” In the examples above, the Super Rich might prefer to ask questions like:

- What is the likelihood that the deal closes?

- What is the probability that I will be offered the position?

- How likely is it that the client buys?

That might sound like too subtle a shift—but this shift to probabilistic thinking potentially can have a big impact on future success.

Determinants of Professional Success

It’s important to realize that there are two major determinants of most professional success: the quality of the decisions you make and luck.

Many people love to emphasize the first while completely discounting the second. Seeking control—and usually being in a position of power—they resist the idea that events might not unfold as they envision them.

The idea that there is a high degree of certainty when it comes to their business lives, or to their lives in general, can be very appealing—but it’s very often inaccurate.

This misperception is seen much less frequently among the self-made Super Rich, however. They, by and large, recognize that there are numerous factors that can make or break a business endeavor and that many of those factors are beyond their control. Quite often, luck needs to be present for things to go their way.

For the self-made Super Rich, the emphasis is on making quality decisions as consistently as possible—and then they hope to get lucky so the vast world beyond their control will turn in their favor.

Of course, quality decisions are within their control. So their aim is to be as adept as possible at making such decisions—which often entails thinking in terms of probabilities.

Bad Lessons Learned

Because so many people crave order and certainty even where neither exists, they tend to draw direct lines between outcomes and causes—after the fact (hindsight being 20/20, as they say). This happens on the positive side and the negative side of the decision-making ledger. Here are some examples.

Positive:

- We nailed it. There was no way the new product could have not been a tremendous success.

- I’m the best candidate, so how could they not offer me the job?

Negative:

- The signs of the Great Recession were like a big, flashing red light.

- There was no way the other company would have gone for the deal.

This is known as hindsight bias, when everything is so very clear in retrospect. Due to hindsight bias, people often make a tight connection between the decisions they made and the outcomes they achieved (mostly when things worked out favorably).

Think about some of the more important decisions you have made—personal, professional or perhaps both—that turned out very well and some that went not so well. Now ask yourself:

- Was the reasoning behind those decisions faulty?

- Was the information I had at the time inaccurate?

- Were my goals at the time unrealistic?

When people go through this type of self-reflection exercise, they often find that they made quality decisions. And yet, some situations turned out great and others did not. In short, factors other than the quality of the decision-making process greatly impacted the outcome. These factors are typically unknown and outside their control—aka luck.

Embracing Uncertainty

It is hard for many people to say “I’m unsure” or “I don’t know.” That’s often especially true among people who generate significant success in life and business. Unpredictability commonly runs counter to the ideas of business certitude and sheer force of will.

Wisdom is said to be learning well from experience. Being able to discriminate between quality decisions and luck when it comes to outcomes can help you become wise. And ultimately, being wise potentially can make you a better decision-maker. As decisions are predictions of the future, the more practice you have—coupled with an honest assessment of the extent to which the decisions you made produced the outcomes you achieved—will only enable you to be more capable going forward.

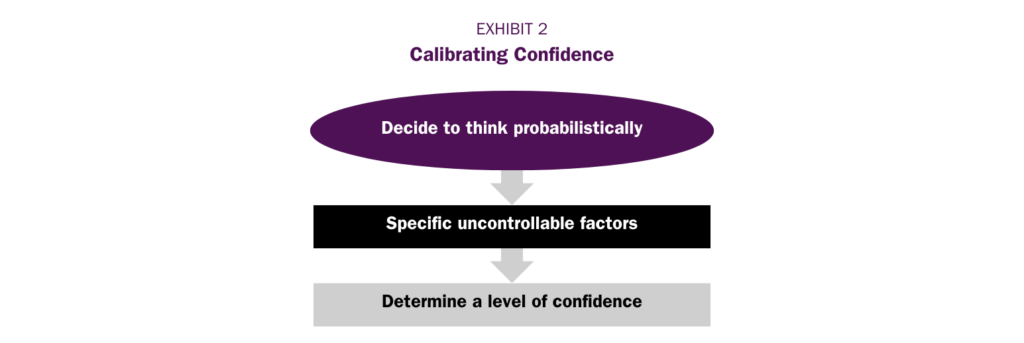

Essentially, you want to calibrate your confidence. The first step in doing so is to decide to think in probabilistic terms. Then you specify as many uncontrollable factors as possible (without getting absurd about it). For example, you cannot control the geopolitical environment in the world. But you can take an informed guess about its effect on a business decision. Then you determine a level of confidence in the outcome. This calibration process is summarized in Exhibit 2.

Part of this process involves scenario thinking, which is essentially a method of generating alternative futures. It’s the point where all the “what if” questions are asked and answered.

Some examples:

- “What if the company is acquired by a competitor and eliminates what they deem to be redundancies?”

- “What if the client is ready to move forward much faster than we’re anticipating because they get the funding they seek?”

- “What if I want to expand my business to other countries and want to legally minimize the amount of taxes I will have to pay?”

- “What if both of our daughters get accepted to their first-choice colleges?”

There are a number of different ways to deal with each of these matters. From the meaningful possible outcomes devised in this phase, the most viable course or courses of action can be selected.

By thinking this way, you can reframe situations in more insightful ways. Consider the earlier situations; you might reframe them as:

- There’s a 30% likelihood of getting the sale.

- We have a 50% probability of closing the deal.

- I have somewhere between a 60% and an 80% chance of getting the job.

This approach can make your decision-making much more realistic. You can use your experience and the insights you have gained along the way to improve your knowledge of the situation—thereby enabling you to make superior choices.

Important: Ignoring uncertainty and related risks can potentially reduce your anxiety, but doing so is probably going to impair the quality of your decision-making. By admitting and recognizing uncertainty and working to address it, you may find yourself better positioned to take actions that can give you a greater chance of achieving your agenda.

What to Do if Things Look Bad

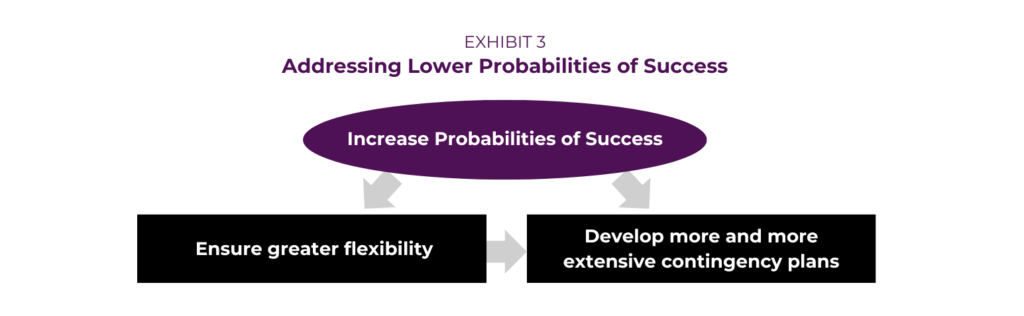

Based on your level of uncertainty, you can take a few actions to increase the probability that you will achieve the outcomes you are looking for. There are two fundamental and related ways of doing this (see Exhibit 3).

One approach is to build more flexibility into your plans. That way, as the situation progresses, you can make adjustments to help keep the endeavor pointed in the right direction.

Another approach is to develop a number of contingency plans. When luck is not on your side, you can shift to alternative versions of the endeavor that you believe have a higher likelihood of getting the results you want. Contingency planning is all about developing alternative scenarios with somewhat different action steps that you believe will help you reach your goals. Each possible future—each contingency—has its own advantages and disadvantages. There are rarely simple answers when planning for various contingencies, so you always have to be assessing how things are progressing in order to make adjustments when appropriate.

Conclusion

By shifting your decision-making mindset to focus not on whether something will definitely happen but rather on the likelihood of something happening, you give yourself more flexibility and a greater ability to make smart decisions. You also factor in one of the more powerful drivers of results for everyone: luck.

VFO Inner Circle Special Report

By John J. Bowen Jr.

© Copyright 2024 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including but not limited to electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees. This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the author nor the publisher may be held liable in any way for any interpretation or use of the information in this publication. The author will make recommendations for solutions for you to explore that are not his own. Any recommendation is always based on the author’s research and experience. The information contained herein is accurate to the best of the publisher’s and author’s knowledge; however, the publisher and author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Nathan Brinkman is a registered representative and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC (www.sipc.org) Supervisory office: 8888 Keystone Crossing #1600, Indianapolis, IN 46240 (317) 469-9999. Triumph Wealth Management, LLC is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Nathan Brinkman: CA Insurance License #0C27168 CRN202709-7228059