Key Takeaways

- The ultra-wealthy tend to enjoy saving money over spending it.

- They also often want to be involved in the day-to-day aspects of investing.

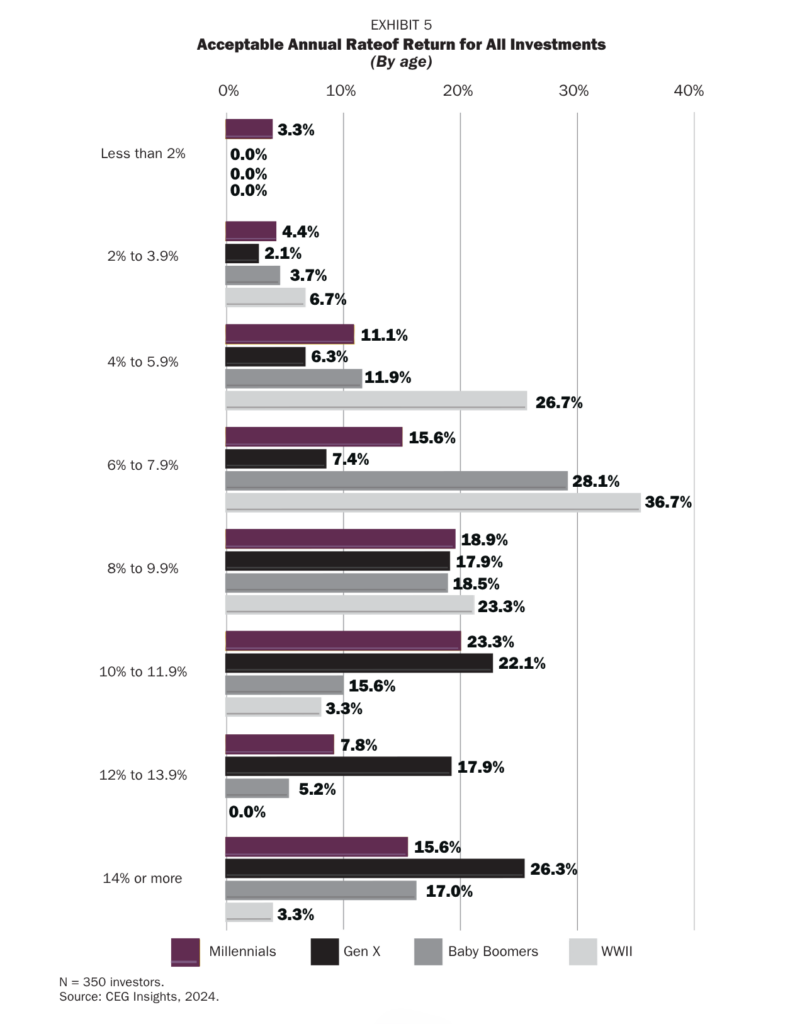

- Almost one-fifth expect investment returns of 14% or more annually.

Given their level of affluence, it’s not surprising that the ultra-wealthy—those investors with a net worth of $25 million or more (not including primary residence)—have some strong opinions about investing.

If you’re a member of this group, you may very well want to know your peers’ thinking in this key area of wealth management. But even if your net worth is significantly less than $25 million, it can be interesting and potentially helpful to discover how the ultra-wealthy invest—their perspective on assets, their expectations for returns and other key factors.

With that in mind, CEG Insights surveyed 350 ultra-wealthy investors—asking them about their assets, their risk tolerance, their investment attitudes and behaviors, and more. Here’s what they had to say.*

*CEG Insights, The $25 Million+ Investor, 2024.

Assets

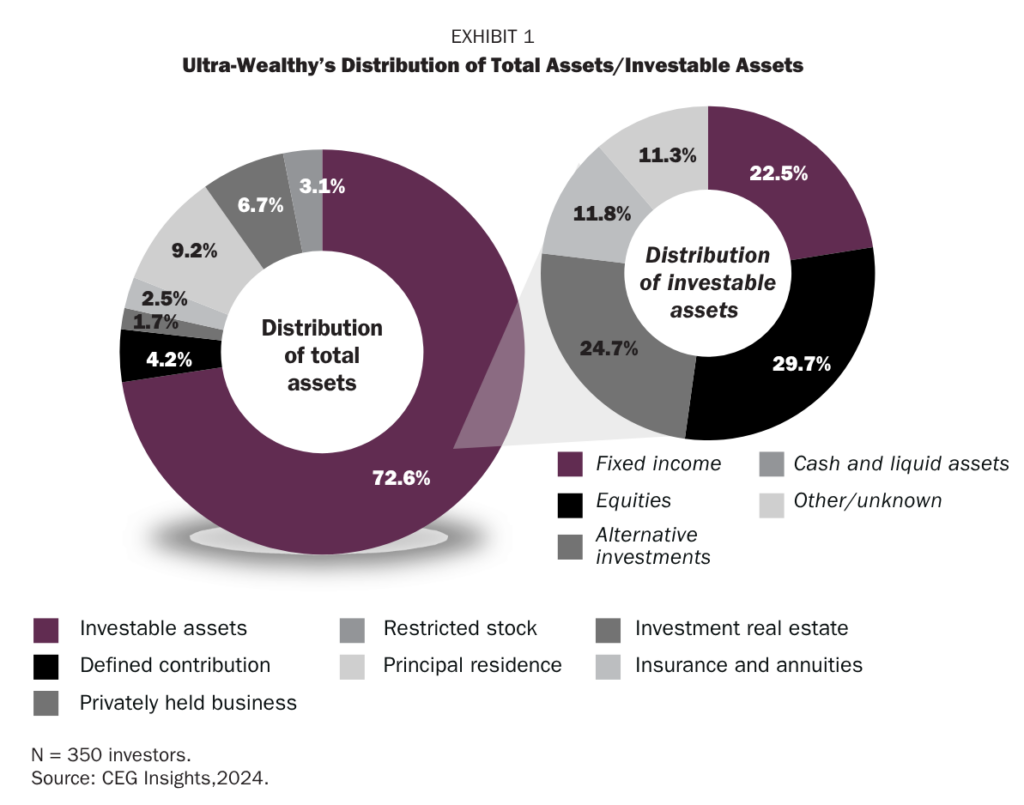

How do the ultra-wealthy invest? A few key findings, summarized in Exhibit 1 on the following page, include these:

- Investable assets play a major role. Ultra-wealthy households allocate the majority of their wealth to investable assets, which represent 72.6% of their total holdings. This highlights the importance of liquid, growth-oriented and income-generating investments within their portfolios.

- Stocks are especially popular. Equities, which make up 30% of these investable assets, are the single largest asset class. This allocation underscores the confidence many high-net-worth investors have in equity markets as a primary source of long-term growth. Equities’ significant share also suggests that affluent investors are willing to accept market volatility in pursuit of higher returns.

- Alts are also in demand. Alternative investments—including hedge funds, private equity and real assets like commodities—constitute nearly a quarter of the investable asset mix (24.7%). The robust allocation to alternatives reflects a desire to diversify away from traditional stocks and bonds.

- Other investable assets remain important. In terms of fixed income, this asset class represents over 20% of investable assets, indicating that even wealthy investors prioritize income stability and risk mitigation through bonds and similar securities. The preference for fixed income likely suggests a balanced approach to managing wealth, where capital preservation and income generation are critical, especially as investors near retirement or during periods of market uncertainty. Meanwhile, cash and liquid assets account for more than 11% of investable assets. This allocation may indicate that many wealthy individuals prefer to maintain liquidity for flexibility, whether for opportunistic investments or unforeseen expenses, or it may be a reflection of a cautious market outlook.

- Homes play a small role. When considering total assets, principal residences account for less than 10% of the overall portfolio (2.5%). While homeownership remains an important part of the financial landscape, for affluent households, real estate—specifically primary residences—may not be as central to wealth accumulation as investable assets. This finding suggests that high-net-worth individuals may view their homes more as lifestyle choices rather than primary vehicles for wealth growth.

Risk tolerance

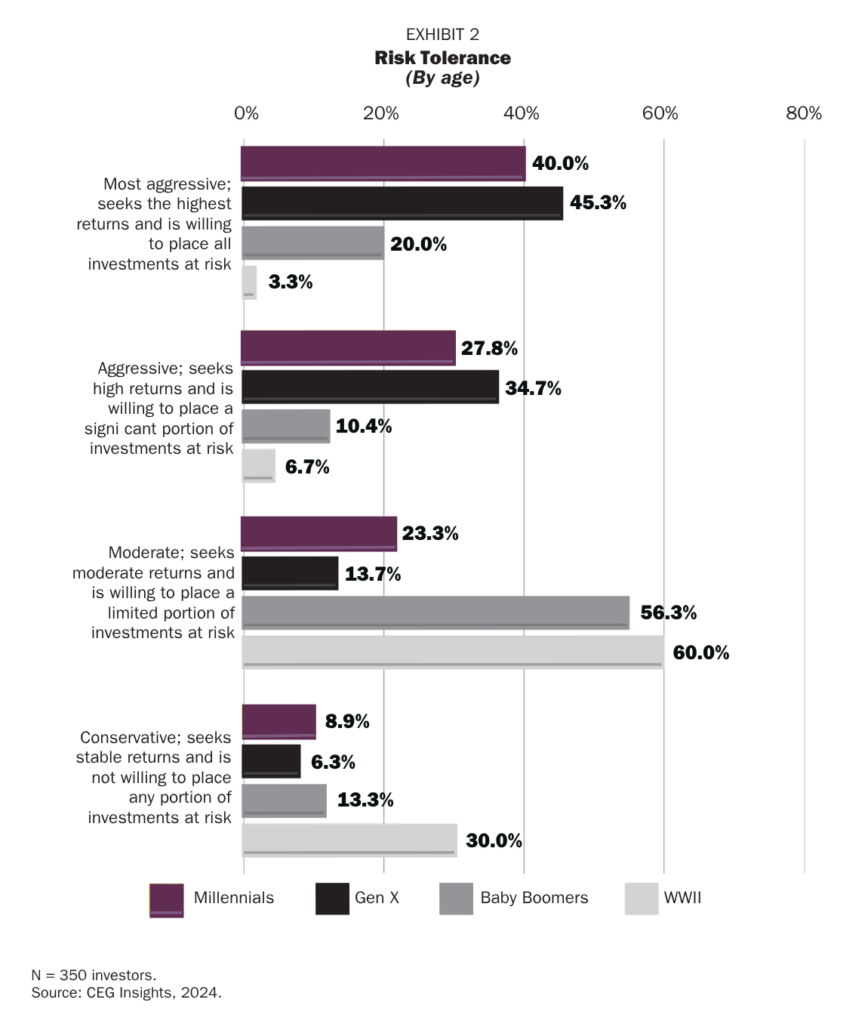

Understanding risktolerance offers insight into how the ultra-wealthy approach investment decisions. More than a third of these investors describe their risk tolerance as “moderate.” Another 30%, however, describe their risk tolerance as “most aggressive.” Note, in Exhibit 2, that Gen X investors are more likely than Millennials to describe their risk tolerance as “aggressive” or “most aggressive.” Not surprisingly, Baby Boomers and WWII investors tend to be moderate investors. (See Exhibit 2.)

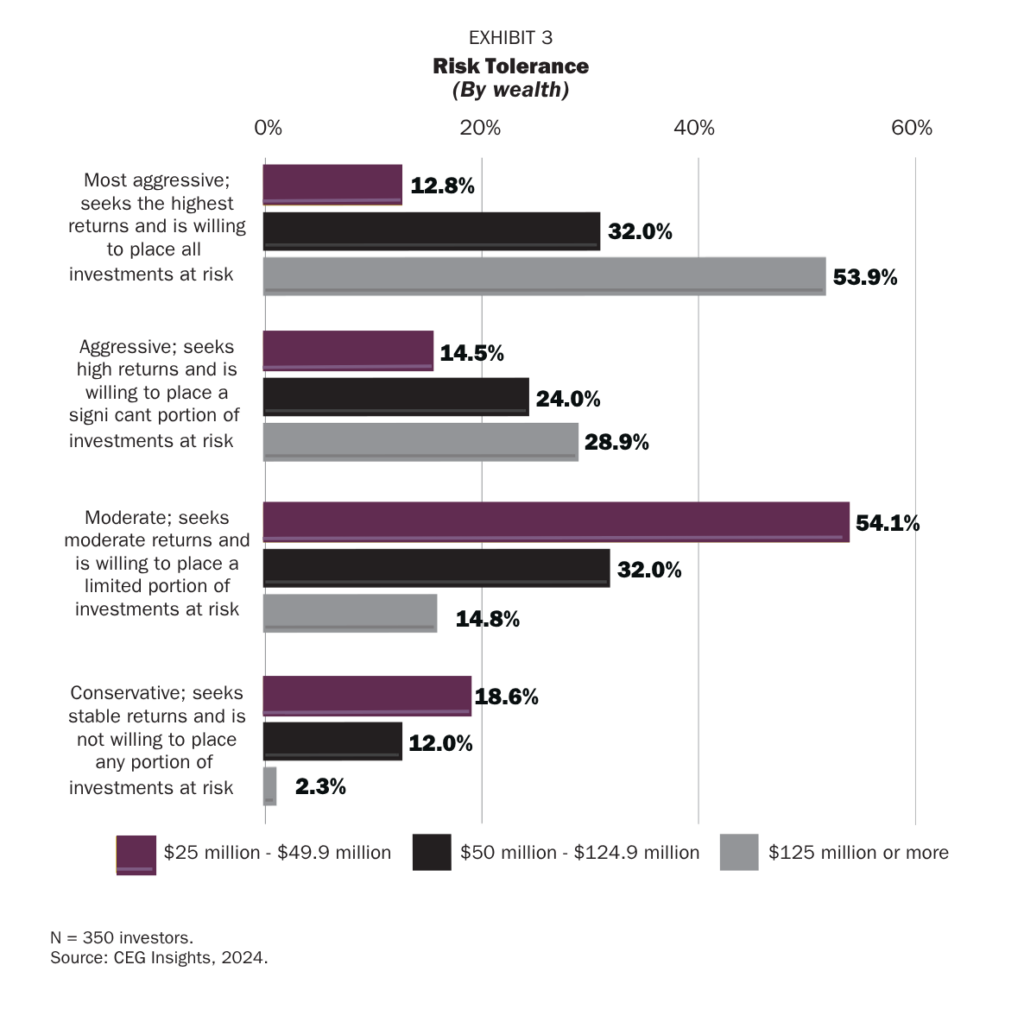

Additionally, as Exhibit 3 shows, the wealthiest investors tend to have the most aggressive risk tolerance, while those who are less wealthy tend to be more moderate.

Financial behaviors and involvement

Risk tolerance informs investment strategy, but it’s equally important to consider how $25 million+ investors prefer to manage their wealth on a daily basis. For example:

- More than three-quarters of wealthy households—76.9%—find greater satisfaction in saving and investing than in spending, indicating a strong inclination toward preserving and growing their wealth.

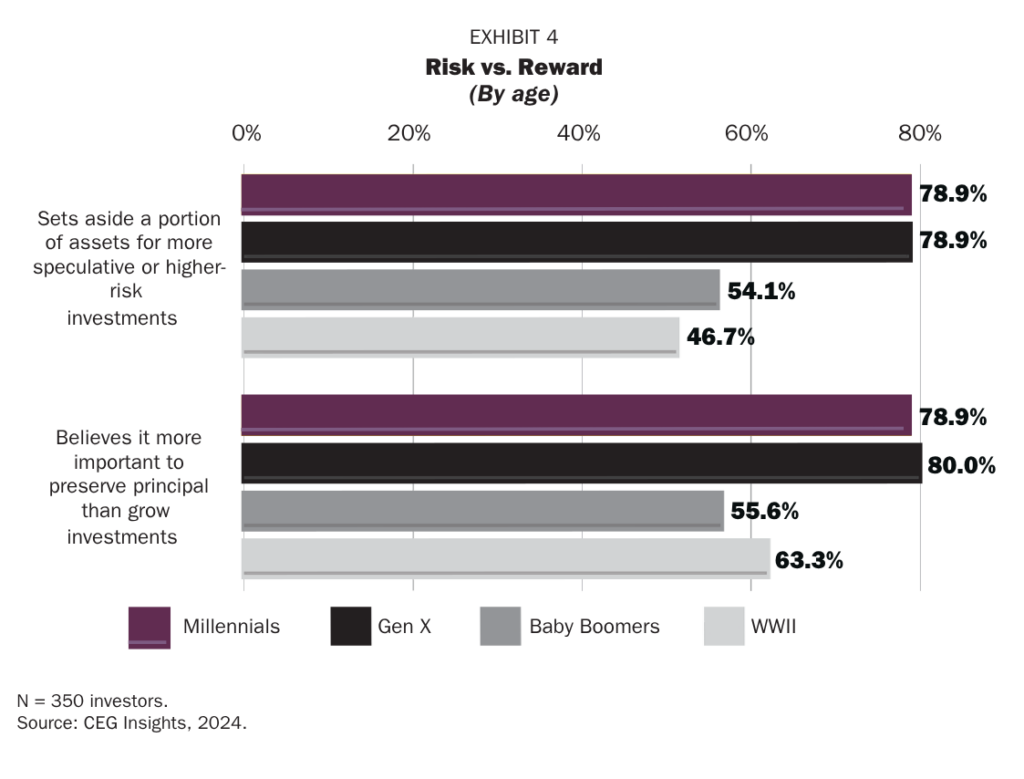

- What’s more, two-thirds of investors want to set aside some of their money for more speculative or higher-risk investments.

Are $25 million+ investors more interested in wealth preservation or asset growth? The research found that both of these goals are important to investors, regardless of age (see Exhibit 4).

More than two-thirds of wealthy investors like to be actively involved in the day-to-day management of investments, and the same percentage indicate that they enjoy investing and don’t want to give it up. The wealthiest investors are the most likely to want to be involved in the day-to-day investment of their assets. Gen X investors (83.2%) also want to be involved with their investments on a daily basis, as do 78.9% of Millennials. But only 50.4% of Baby Boomers want daily involvement.

Investment expectations

The ultra-wealthy investors surveyed have varied expectations for acceptable annual returns, with the largest group (20%) aiming for between 6% and 7.9% (see Exhibit 5), while significant portions expect higher returns of between 8% and 9.9%, or 10% and 11.9%. Notably, 18% expect returns of 14% or more.

While older investors are more likely to expect a rate of return between 6% and 7.9%, younger investors have higher expectations—the largest percentage of Gen X investors expect a return of 14% or more. The wealthiest investors feel the same.

How do you compare?

These insights into the ultra-wealthy can serve as a jumping-off point to examine your own investment preferences and expectations. For example, ask yourself questions such as:

- What annual rate of return on my overall portfolio is acceptable, given my goals?

- Are my investable assets allocated appropriately based on my return expectations, risk tolerance and other factors?

- How involved do I want to be in the investment process, and what do I want that involvement to look like?

- Am I spending money in ways that give me satisfaction, or would I be happier if I saved more money than I currently do?

You may find that you’re highly aligned with the views of the ultra-wealthy outlined above— or you may feel very differently about some of these issues. Regardless, taking steps to increase your clarity about your investing and some of the drivers behind the decisions you make about your wealth can potentially be helpful and rewarding in the months and years ahead.

VFO Inner Circle Special Report

By John J. Bowen Jr.

© Copyright 2026 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including but not limited to electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the author nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The author will make recommendations for solutions for you to explore that are not his own. Any recommendation is always based on the author’s research and experience.

The information contained herein is accurate to the best of the publisher’s and the author’s knowledge; however, the publisher and the author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Nathan Brinkman is a registered representative and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC (www.sipc.org) Supervisory office: 8888 Keystone Crossing #1600, Indianapolis, IN 46240 (317) 469-9999. Triumph Wealth Management, LLC is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Nathan Brinkman: CA Insurance License #0C27168 CRN202903-10801421