Key Takeaways

- Most ultra-affluent households say they get greater satisfaction from saving and investing than from spending, according to CEG Insights.

- Overall, the ultra-affluent claim to have a high tolerance for investment risk—but also report being more focused on protecting wealth than on growing it, according to CEG Insights.

- The ultra-affluent by and large like to be actively involved in the area of investment management—even if they work with professionals, according to CEG Insights.

It seems that no matter how wealthy we may be, we occasionally like to peek into the next level of affluence and see what even wealthier people are doing with their money. Perhaps we’re feeling aspirational and want to know what our lives might look like if we reach that level someday. Maybe it’s just idle curiosity.

Regardless of the reason, getting to know the thoughts and actions of people who have achieved significant financial success has the potential to benefit us on our own financial journeys.

With that in mind, we’re taking a look at some key attitudes, beliefs and behaviors of the wealthiest households in the United States—those with at least $25 million in net worth, not including the value of their primary residences—using data from a survey conducted by CEG Insights. We call them the ultra-wealthy. All respondents were the primary decision-makers for day-to-day financial issues in their households.1

Keep in mind that these findings aren’t endorsements or recommendations—simply insights into this particular wealthy group. Your own goals and attitudes—and the “right” plan for your wealth—will depend on your unique situation.

1 Source of all data on the ultra-wealthy (defined as individuals with at least $25 million in net worth, not

including value of primary residences) cited in this report: CEG Insights, The $25 Million+ Opportunity, 2023.

Who are the ultra-affluent?

Entrepreneurship is a common trait among those with $25 million or more in net worth. Consider that among all respondents, almost six in ten—58.1%—indicated that they are business owners. A little over one-third are senior executives/managers.

The upshot: Business ownership can be a key driver of financial success for the wealthiest among us. One study by The University of Chicago Booth School of Business found that most individuals on the Forbes 400 list of wealthiest Americans made their own fortune and that the percentage who started their own business rose over time from 40% to 69%.2

What’s more, nearly half of respondents—46.1%—are working but preparing for retirement. Around 16% are fully retired and engaged in other activities, such as volunteering or traveling.

Attitudes toward saving

In a finding that should surprise no one, the vast majority of the ultra-wealthy (78.6%) say their happiness stems in large part from the wealth they have accumulated. These investors might argue that, in fact, money can buy happiness.

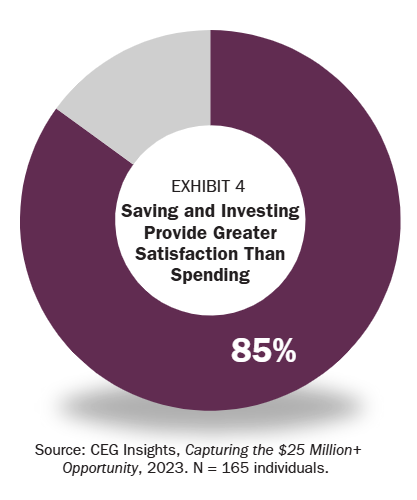

But what may be more interesting: Not only does their wealth make these investors happy, but so do saving and managing their money (see Exhibit 4). Nearly 85% of these investors report that they get greater satisfaction from saving and investing than from spending. (At the highest wealth level studied—$125 million or more—it’s even higher, at 92.1%.)

2 Steven N. Kaplan and Joshua D. Rauh, ”Family, Education, and Sources of Wealth Among the Richest Americans, 1982–2012.” American Economic Review Papers & Proceedings, May 2013.

Attitudes toward spending

While the ultra-affluent (by and large) value saving money over spending it, that doesn’t mean they’re all a bunch of Scrooges.

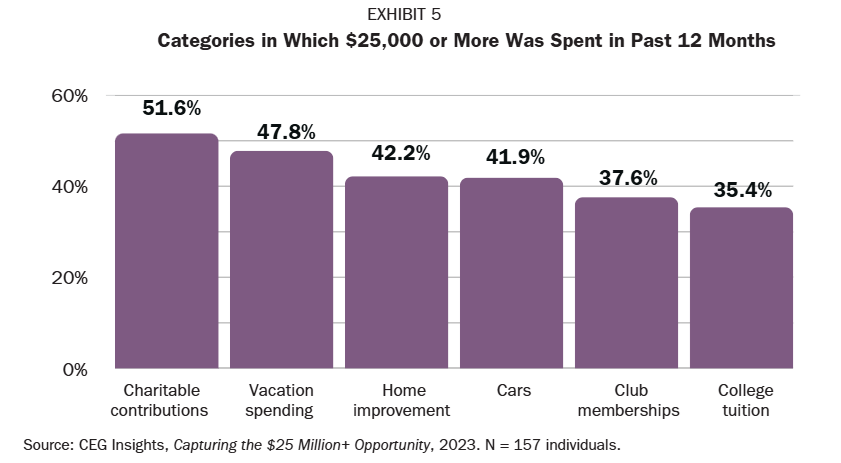

If we look at significant annual spending—$25,000 or more—charitable donations are the top expenditure for this group, with slightly over half (51.6%) donating at least $25,000 to charity. One in eight (15.3%) donated more than $100,000 in the past year. (See Exhibit 5.)

In second place—and very close behind—is vacation spending: 47.8% of respondents spend at least $25,000 on vacations annually. Home improvement was another significant expenditure, with 42.4% spending $25,000 or more over the past 12 months on improvements. Other areas where respondents spent at least $25,000 annually include cars (41.9%), club memberships (37.6%) and college tuition (35.4%).

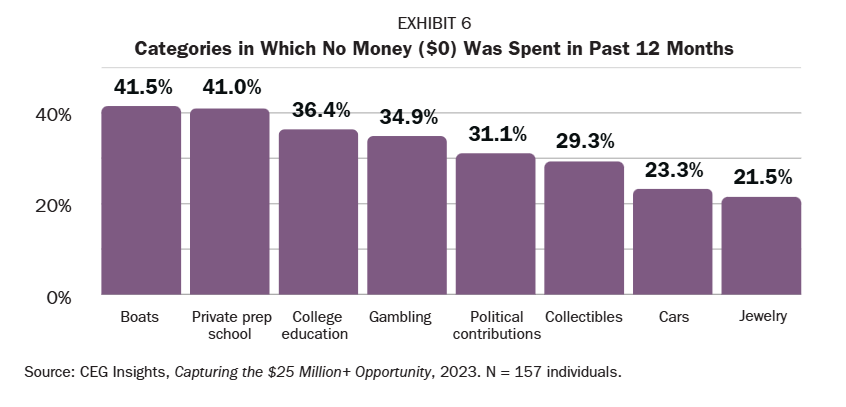

Interestingly, more than 20% of these ultra-wealthy investors do not spend a single dollar on many items commonly associated with the wealthy in popular culture: cars, boats, jewelry, collectibles, gambling and political contributions. In addition, 41% spend nothing on private prep schools (see Exhibit 6).

A look at the ultra-wealthy’s investments

How do the ultra-wealthy invest? Investable assets make up an average of 73.5% of the total household assets of the ultra-wealthy. In looking at the investable assets, we see that just under 30% are equities, slightly less than one-quarter are alternative investments and 22.3% are fixed-income investments. Rounding out the distribution of investable assets are cash and other liquid assets (11.4%) and other or unknown (11.7%).

Outside of investable assets, nearly 9% of their total assets consist of investment real estate, while 6.7% consists of insurance and annuities. Small percentages consist of things like restricted stock and privately held businesses.

Conflicting signs about tolerance for investment risk

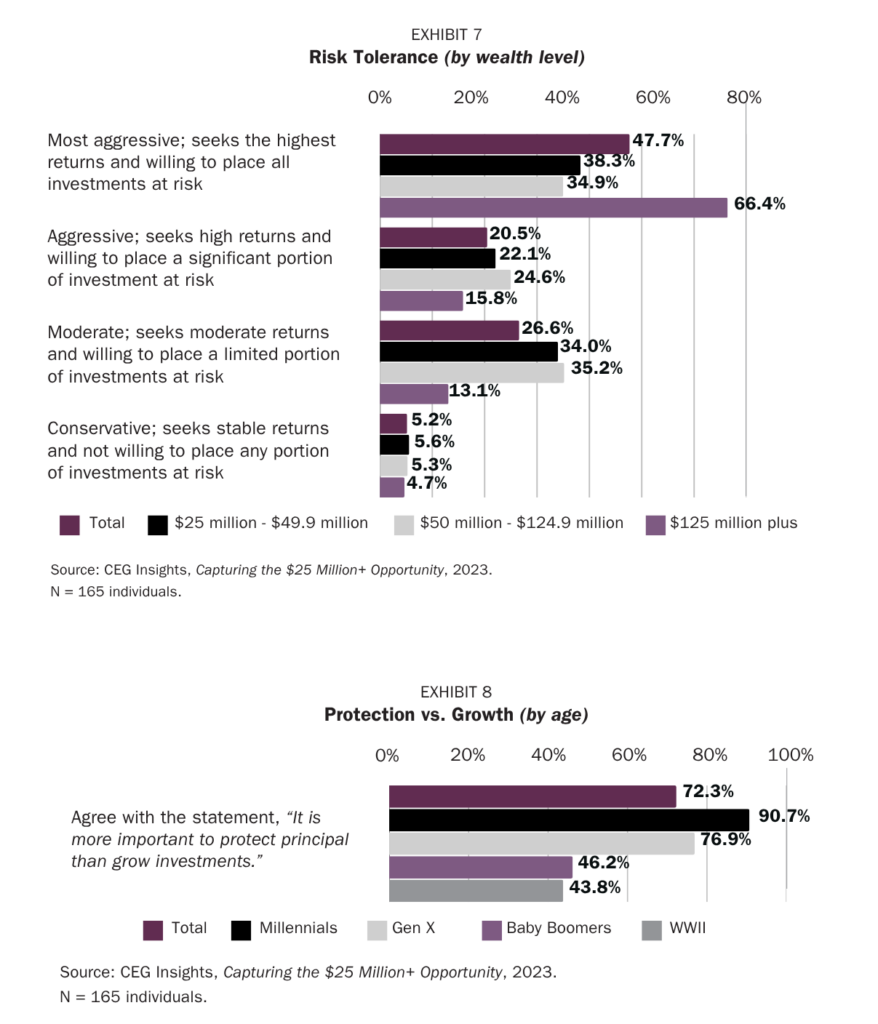

The ultra-wealthy have widely differing levels of tolerance for risk. That said, most of them seem to be quite comfortable taking on risk:

- Nearly half (47.7%) report a highly aggressive approach, with a smaller yet substantial group (20.5%) adopting a somewhat less aggressive stance.

- A cautious contingent (26.6%) prefers a moderate path, while a small group (5.2%) favors a safe, conservative approach.

Not surprisingly, perhaps, age plays a significant factor in the amount of risk these investors are willing to tolerate. The younger investors, who have the most time to recover losses, are the most willing to place all of their investments at risk. Six in ten millennials (59.8%) and two-thirds of Gen Xers (66.7%) characterize their risk tolerance as most aggressive. At the other end of the age spectrum, 75.1% of the WWII generation are either moderate (68.8%) or conservative (6.3%).

But given how wealthy these investors already are, it may seem surprising that so many report having a high risk tolerance (see Exhibit 7). In fact, among the wealthiest of the ultra-wealthy—those with $125 million or more—fully two-thirds (66.4%) put themselves in the “most aggressive” category.

The idea that the ultra-wealthy are extremely risk-tolerant is challenged, however, by another finding: 72.3% of these investors said that they would rather protect what they have accumulated than take risks to grow their investments (see Exhibit 8).

Managing investments

One thing that does seem clear: Ultra-wealthy investors don’t want to take a backseat when it comes to their investing. They want to be at the steering wheel—or at least have their hands on it.

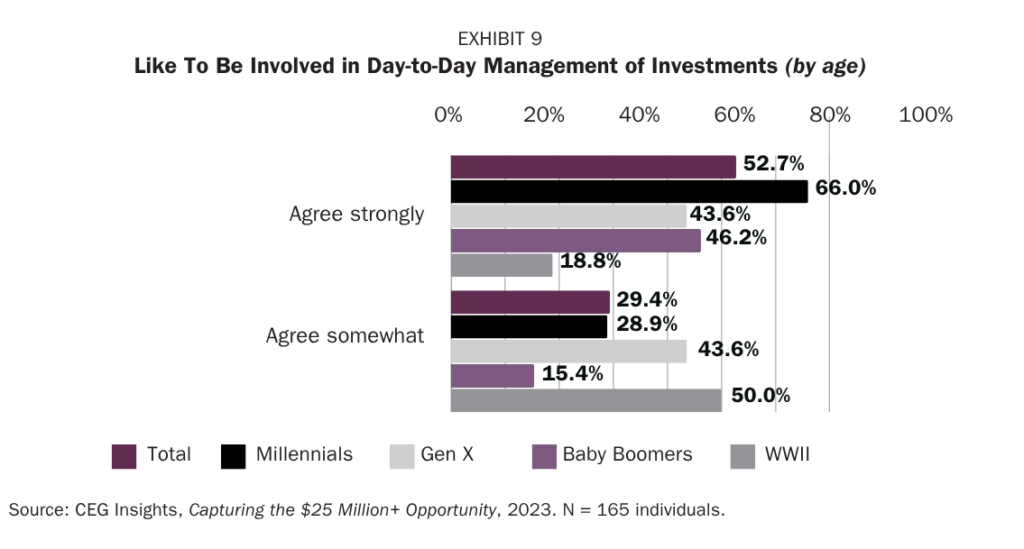

For example, 82.1% want to be actively involved in day-to-day investment management. Among ultra-wealthy millennials, this desire is nearly universal—reported by 94.9% of this age group (see Exhibit 9). In addition, 79% of ultra-wealthy investors overall say that they enjoy investing and do not want to give it up.

This flies in the face of the assumption many people make that the very wealthy outsource or “farm out” all the challenging aspects of their lives to experts in order to reduce “friction points.” Instead, the ultra-affluent find the investing process interesting and intriguing enough to participate in it. They do so in a few key ways:

- Many of these ultra-wealthy investors conduct their own investment research. Three-quarters (74.5%) do online research to evaluate, while nearly half (47.6%) consult with their advisor on these opportunities.

- A similar number (45.6%) read annual reports.

- Just over a third (36.5%) look at past performance.

Next steps

Consider using this look at the ultra-wealthy as an opportunity to examine some of your own views and actions in key areas of your financial life—such as spending, saving, investing and risk-taking. For example:

- Entrepreneurship. Business ownership is often a risky proposition—but the research shows that the majority of the ultra-affluent put themselves in the line of wealth by owning businesses.

- Spending. How does your spending compare to that of the ultra-affluent? Sure, you might not contribute $25,000 or more annually to charity or vacations, but do you actually know where the bulk of your spending goes? Some research suggests that spending on experiences and in ways that help others can potentially boost our happiness3—so it’s noteworthy that the ultra-affluent allocate so much of their savings to philanthropy and vacations, for example.

- Investing. When it comes to investing, are you as involved in the process as you’d like to be—and where do you go for insights about financial markets?

3 Paulina Pchelin and Ryan T. Howell, “The hidden cost of value-seeking: People do not accurately forecast the economic benefits of experiential purchases,” The Journal of Positive Psychology, March 31, 2014.

VFO Inner Circle Special Report

By John J. Bowen Jr.

© Copyright 2025 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including but not limited to electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the author nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The author will make recommendations for solutions for you to explore that are not his own. Any recommendation is always based on the author’s research and experience.

The information contained herein is accurate to the best of the publisher’s and the author’s knowledge; however, the publisher and the author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof. Unless otherwise noted, the source for all data cited regarding financial advisors in this report is CEG Worldwide, LLC. The source for all data cited regarding business owners and other professionals is AES Nation, LLC.

The information contained herein is accurate to the best of the publisher’s and the author’s knowledge; however, the publisher and the author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Nathan Brinkman is a registered representative and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC (www.sipc.org) Supervisory office: 900 E 96th St. Ste 300, Indianapolis, IN 46240 (317) 469-9999. Triumph Wealth Management, LLC is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Nathan Brinkman: CA Insurance License #0C27168 CRN202803-8322140