Key Takeaways

- Donating a life insurance policy is one way to potentially increase the size of a charitable gift you make.

- You can name a charity as the beneficiary of your policy— or make the charity itself the policy owner.

- Gifting the policy dividends is another approach to consider.

People purchase life insurance for lots of reasons—the most common often being to take care of their loved ones. The life insurance proceeds are used either to create an estate for those left behind or to pay taxes so the family receives the estate. Still others might use life insurance to maximize income (such as by supercharging a retirement plan) or to address business concerns (as in the form of providing company benefits).

But did you know you can potentially use life insurance to leave a charitable legacy?

Life insurance can be an effective way to help the causes you care about by providing the payout from a policy to a charitable organization. Typically, the life insurance death benefit will significantly exceed the premiums paid for the life insurance policy—thus allowing you to make a much larger gift than might otherwise be possible.

Here’s a look at how it works.

An overview

The use of life insurance to fund a charitable organization might appeal to you if, for example, you find that you don’t have beneficiaries who are in need of the money from the policy.

Perhaps the biggest advantage of donating a life insurance policy is leverage; it is a way to increase the size of a charitable gift. In some cases, it is also a way for donors to receive a greater tax deduction than they’d receive donating cash.

Both term and permanent life insurance policies can be donated to charity. However, permanent insurance is typically used for donations because it’s not in force for only a certain number of years (as is the case with term life). This way, the gift can eventually be made even if the donors live very long lives. Another advantage of using a permanent life insurance policy: The charitable organization can surrender the policy for cash if it owns the policy before the donor dies.

What’s more, you can name practically any charitable organization as the life insurance policy’s beneficiary—although it’s always smart to double-check that any charity you’re considering supporting will accept a life insurance donation. That means educational institutions, religious organizations and health care-related charities, among others. The options There are a number of ways you can donate a life insurance policy to charity. These different approaches have different tax implications for you as the donor (see Exhibit 1). Therefore, it’s a good idea to seek the advice of a tax professional when making donations of life insurance policies.

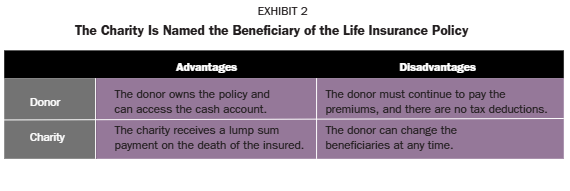

Option 1: The charity is named the beneficiary of the life insurance policy

When you name the charity as the beneficiary, the charity gets the death benefit when you (as the donor) die. This is not an all-or-none scenario, though. Because you retain ownership of the policy, you can name multiple beneficiaries—such as a number of loved ones and one or more charitable organizations. You can name a charity as a beneficiary by purchasing a new life insurance policy or adding the charity as a beneficiary on an existing policy.

Another feature of naming a charity as a beneficiary: It keeps the matter private, which might be important if you don’t want to reveal your intentions to heirs.

Important:

In many situations, with an existing life insurance policy, it is fairly easy to change or add beneficiaries. However, some life insurance companies can limit the option of making a charity a beneficiary.

Some of the advantages and disadvantages/risks of this approach are shown in Exhibit 2.

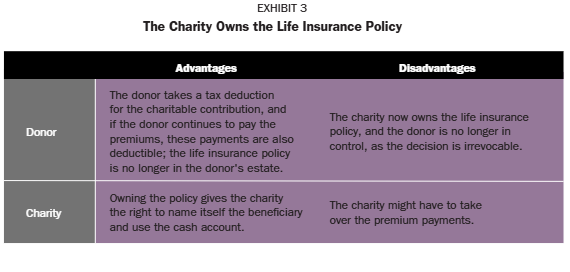

Option 2: The charity owns the life insurance policy

Alternatively, you (as the donor) can make the charity the owner of a life insurance policy—a strategy that can generate tax deductions for you. This move also gets the insurance policy out of your estate for tax purposes. The risks, however: Once the charity owns the policy, you’re no longer in control of it—and the decision is an irrevocable one.

This can be done with a new policy or an existing one. In both cases, the charity is named the beneficiary and receives the death benefit when the insured dies.

In the case of a permanent life insurance policy, a charity that owns the policy might not have to wait until the death of the insured to receive money. Instead, the charity can potentially use the money accumulating in the policy. Also, if there are funds in the cash account, there is the possibility of surrendering the life insurance policy for the cash value.

Some key advantages and disadvantages of this approach are shown in Exhibit 3.

Option 3: The donor gifts the dividends of the life insurance policy

With permanent life insurance policies that provide dividends, you as the donor could use dividends that have built up in the policy to make charitable donations. These contributions are tax deductible. You, as the owner, control the life insurance policy, and the charity is not a beneficiary.

Some risks: The payments that a charity receives using this approach may be irregular or inconsistent from year to year, given that dividends can fluctuate depending on circumstances. Also, if the dividend pool is tied to the death benefit, it might lower the death benefit.

Some advantages and disadvantages of this approach are shown in Exhibit 4.

When making any gifts to charity—especially gifts that involve financial products and legal structures—it can be wise to consult with a tax or wealth management professional. This will better enable you to understand your options and help ensure you are making a decision that is right for you and your particular situation.

That said, don’t automatically let tax considerations be the determining factors in giving to charity. The prime motivation for philanthropy should always be to do good. Keep in mind that even with the tax benefits, you are still giving away some of your wealth. The idea is ultimately to support worthwhile causes in the most tax-effective way possible.

So don’t overlook this option. In the end, you might discover that life insurance is an effective way to leave a charitable legacy and benefit financially.

VFO Inner Circle Special Report

By John J. Bowen Jr.

© Copyright 2025 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including but not limited to electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the author nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The author will make recommendations for solutions for you to explore that are not his own. Any recommendation is always based on the author’s research and experience.

The information contained herein is accurate to the best of the publisher’s and the author’s knowledge; however, the publisher and the author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof. Unless otherwise noted, the source for all data cited regarding financial advisors in this report is CEG Worldwide, LLC. The source for all data cited regarding business owners and other professionals is AES Nation, LLC. The information contained herein is accurate to the best of the publisher’s and the author’s knowledge; however, the publisher and the author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Nathan Brinkman is a registered representative and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC (www.sipc.org) Supervisory office: 900 E 96th St. Ste 300, Indianapolis, IN 46240 (317) 469-9999. Triumph Wealth Management, LLC is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Nathan Brinkman: CA Insurance License #0C27168 CRN202808-9282638