Key Takeaways

- Overall, the ultra-wealthy favor religious organizations and hospitals/health care/curative organizations when they donate.

- Some donors establish donor-advised funds and private foundations to facilitate their giving.

- Think about your own charitable values and goals when creating a giving plan.

Charitable giving often plays a significant role in the financial strategies of affluent investors. Philanthropy can potentially enable individuals and families to support causes they care about while simultaneously gaining financial benefits such as tax breaks and tax- advantaged growth of assets (depending on the strategy implemented, of course).

For these and other reasons, charitable giving often is a key component of the wealth plans implemented by the ultra-wealthy—those individuals with a net worth of $25 million or more (not including primary residence). You may not be in a position (yet) to give at the level some of the ultra-wealthy do. But understanding how and why they engage in philanthropy may help you develop clarity and new insights into your own plans for “doing well by doing good.”

With that in mind, CEG Insights surveyed 350 ultra-wealthy investors about their views and actions regarding philanthropy. Here’s what they had to say.

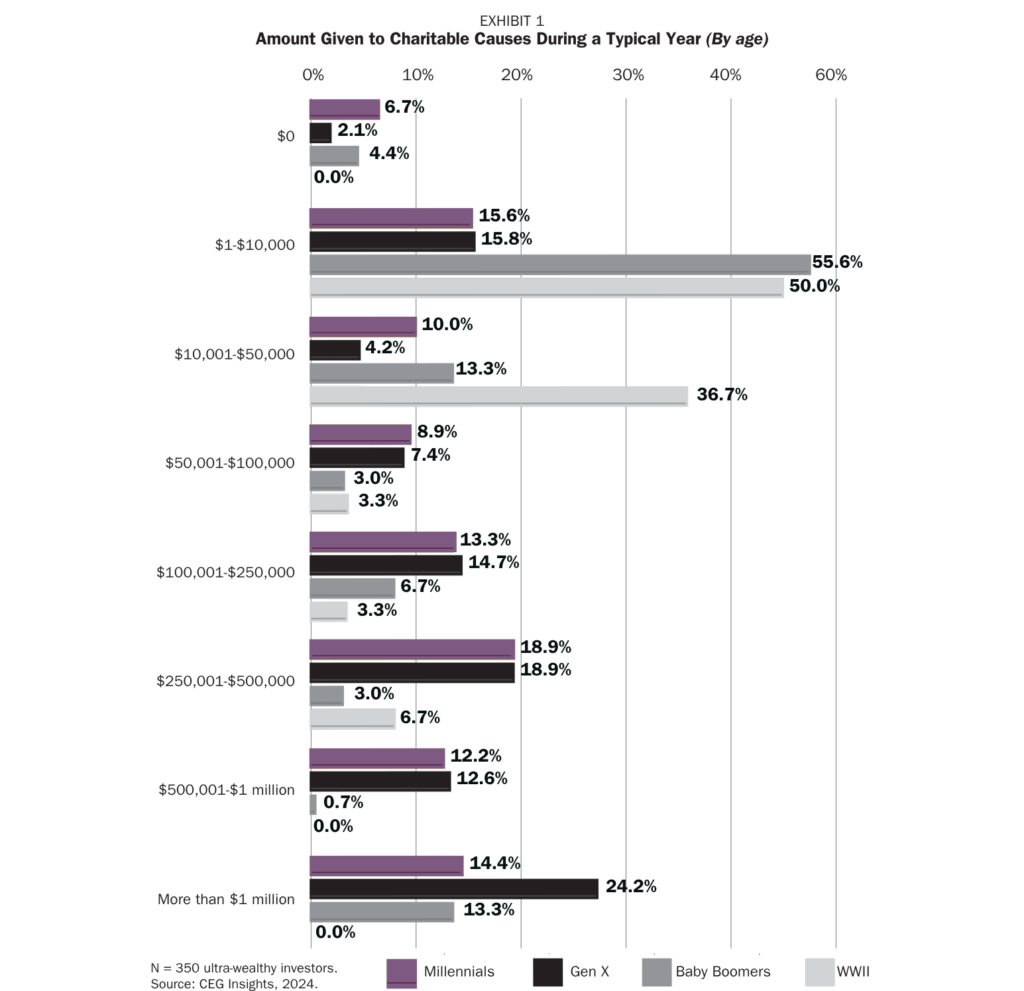

Annual giving habits

A look at giving habits reveals that 34% of the ultra-wealthy give between $1 and $10,000 during a typical year, while 15.4% give more than $1 million annually (see Exhibit 1). Smaller percentages of the ultra-wealthy give amounts somewhere in between those levels. And just 4% don’t engage in philanthropy at all.

However, note that the oldest generations—Baby Boomers and the WWII generation— are the most likely to donate between $1 and $10,000 annually. Meanwhile, a significant percentage of both Millennial and Gen X investors donate more than $100,000 annually.

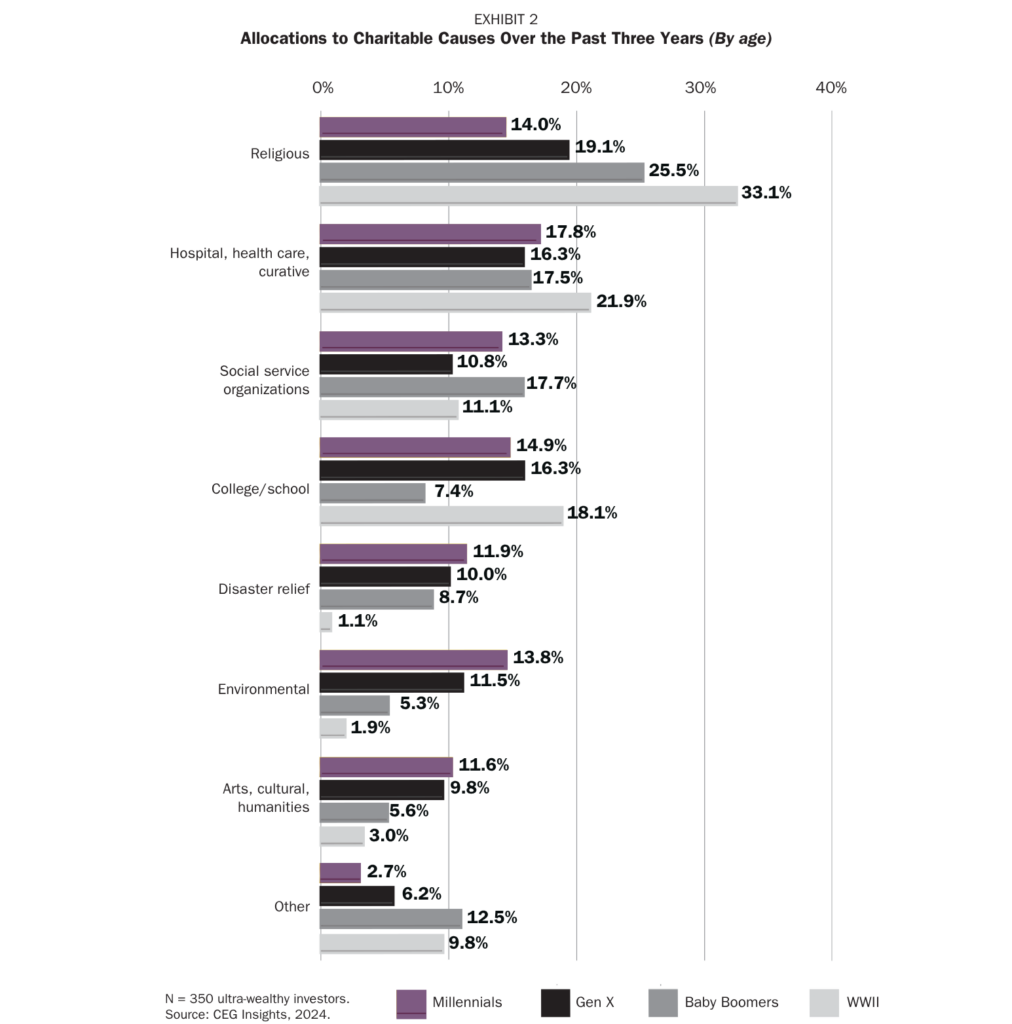

Favored charitable causes

Overall, religious organizations receive the largest percentage of the ultra-wealthy’s charitable donations (21.5%), followed by hospitals/health care/curative organizations (17.6%). Social service organizations (14.1%) and colleges/schools (12.7%) are also important beneficiaries (see Exhibit 2).

Drilling down, however, we see that donors’ age has an impact on the types of organizations to which the $25 million+ segment donates. While more than a third of the WWII generation and a quarter of Baby Boomers donate the most to religious organizations, Millennials are as likely to donate to their college/school, a hospital or a health care organization as to a religious organization.

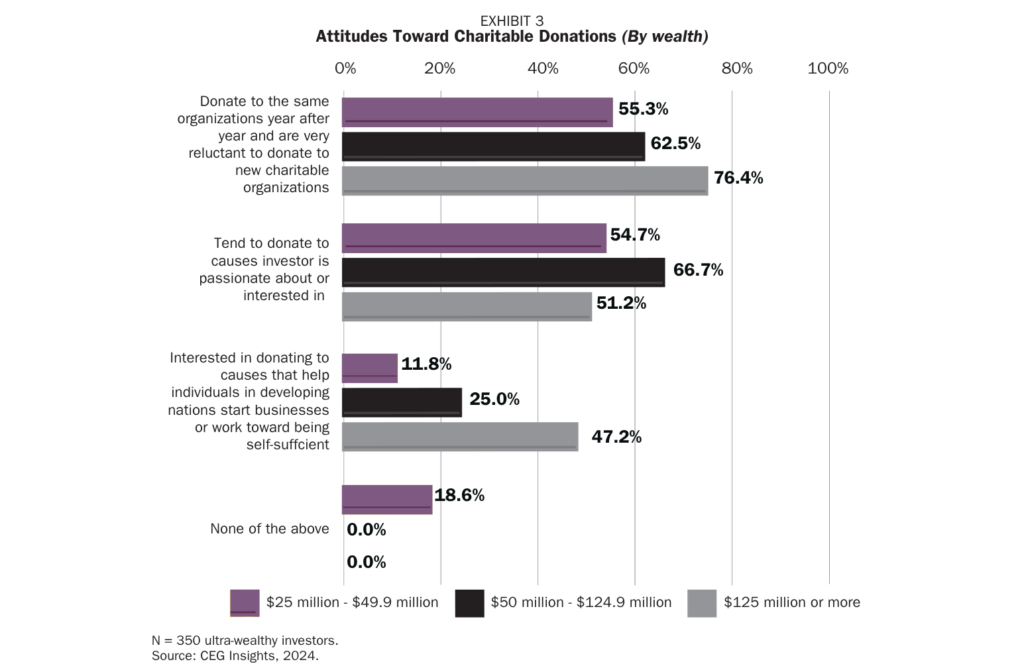

Attitudes toward charitable donations

Beyond the specific causes supported, the underlying attitudes driving charitable giving provide valuable insights into the philanthropic mindset of the wealthy. For example:

- The largest percentage of wealthy households (64.3%) are likely to donate to the same organizations annually and generally donate to causes they are passionate about.

- The wealthiest investors among the ultra-wealthy (47.2%) are more interested than others in donating to causes that help individuals in developing nations start businesses or work toward being self-sufficient.

- Across the board, as seen in Exhibit 3, interest in a cause or charity is a key driver of giving. More than 50% of donors at all wealth levels say they tend to donate to causes they are passionate about or interested in.

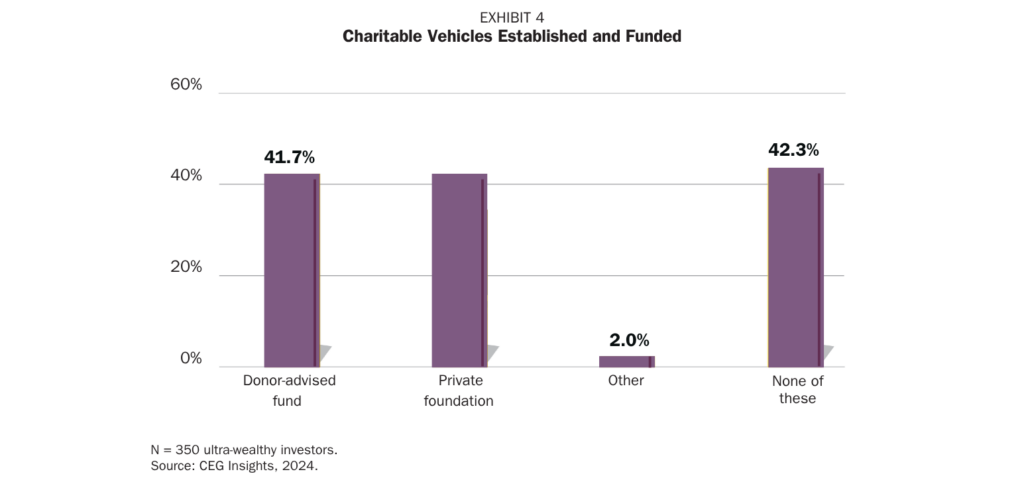

Methods of making donations

While it can be valuable to understand the motivations behind people’s giving, it may be equally important to know which of the various charitable giving vehicles individuals use to facilitate their contributions.

As seen in Exhibit 4, a little more than 41% of the ultra-wealthy have established a donor- advised fund. Close behind, 35.4% have established a private foundation. And yet, even more of the ultra-wealthy (42.3%) have not taken either of these actions.

So how do the ultra-affluent give? Overall, so-called checkbook giving is extremely common (60% overall, with higher percentages among Baby Boomers and the WWII generation). However, younger generations are more likely to create a private foundation or purchase a charitable gift annuity. The wealthiest investors are the most likely to create private foundations or use charitable gift annuities.

Your own planning

There search indicates that the ultra-wealthy overall favor certain charitable giving methods—and that specific subgroups among the ultra-wealthy differ from others in their preferences. As you consider your own charitable plan, consider taking the following steps:

- Formulate your goals. When your giving reflects your deepest values and interests, philanthropy can become powerful and profoundly rewarding. Consider what you care about most and the values you want to convey with your giving. Think about the outcomes you’d like to see your giving help achieve and whether you want your giving to be focused on local issues or worldwide concerns.

- Decide where to give. Identify charitable organizations for helping you achieve your goals. You may decide to deepen an existing relationship with a charity, or you may find that your best route is to identify other organizations. Ask people who are active in the causes that interest you for recommendations, and talk to friends and colleagues who share your charitable interests about the organizations they support. On the internet, websites can be useful both for locating organizations that support your goals and for evaluating them.

- Decide when to give. Consider the timing of your gifts. It could be regular and ongoing annual contributions, or it might be legacy giving through a will or trust. You might also decide to give in response to crises that occur, such as natural disasters.

- Decide what to give. Determine which assets you are willing to invest in pursuit of your charitable goals. It might be cash, tangible property or shares of appreciated stock. Discuss the options with a trusted advisor for the latest rules regarding the tax benefits of donating specific types of assets.

- Consider various giving vehicles. As noted in the research above, there are many methods you can use to engage in philanthropy—each of which has its own rules, advantages and risks. Again, a trusted advisor can review the options and help you find the vehicle or vehicles that are well suited for you based on multiple considerations.

VFO Inner Circle Special Report

By John J. Bowen Jr.

© Copyright 2026 by AES Nation, LLC. All rights reserved.

No part of this publication may be reproduced or retransmitted in any form or by any means, including but not limited to electronic, mechanical, photocopying, recording or any information storage retrieval system, without the prior written permission of the publisher. Unauthorized copying may subject violators to criminal penalties as well as liabilities for substantial monetary damages up to $100,000 per infringement, costs and attorneys’ fees.

This publication should not be utilized as a substitute for professional advice in specific situations. If legal, medical, accounting, financial, consulting, coaching or other professional advice is required, the services of the appropriate professional should be sought. Neither the author nor the publisher may be held liable in any way for any interpretation or use of the information in this publication.

The author will make recommendations for solutions for you to explore that are not his own. Any recommendation is always based on the author’s research and experience.

The information contained herein is accurate to the best of the publisher’s and the author’s knowledge; however, the publisher and the author can accept no responsibility for the accuracy or completeness of such information or for loss or damage caused by any use thereof.

Nathan Brinkman is a registered representative and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC (www.sipc.org) Supervisory office: 8888 Keystone Crossing #1600, Indianapolis, IN 46240 (317) 469-9999. Triumph Wealth Management, LLC is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. Nathan Brinkman: CA Insurance License #0C27168 CRN202908-11141895.